The Future of Essential Health Benefits

By Ian Spatz, Senior Advisor, Manatt Health | Michael S. Kolber, Partner, Manatt Health

Editor's Note: The Essential Health Benefits (EHB) rule may be among the many parts of the Affordable Care Act (ACA) that are on the chopping block as the Trump Administration and Congress seek to repeal and replace the law. The House's proposed American Health Care Act (AHCA) keeps the ten essential health benefits—though it drops the requirement that Medicaid expansion adults receive a benefits package that covers the EHB. The AHCA also would eliminate the requirement for metal level actuarial values but does not eliminate the ACA's maximum annual limit of enrollee cost sharing, which ensures the minimum actuarial value for a plan would not fall substantially below the bronze level currently defined in the ACA. The Trump Administration has indicated it intends to move forward with additional legislative and regulatory changes to ACA requirements, beyond those proposed in the AHCA.

In a recent post for the Health Affairs Blog, summarized below, Manatt Health looks at the origin of EHB, how EHB changed the pre-ACA status quo and what the future could hold. Click here to read the full post.

____________________________________

EHB defines what healthcare benefits plans in the Marketplaces, as well as certain other plans, must cover—and goes to the heart of what it means to have health insurance. Critics cite essential health benefits as a driver of high health insurance costs, claiming that they are too expansive and too prescriptive. Several Republican governors have supported EHB changes in letters to Congress, calling for greater state flexibility and eliminating the federal EHB requirement, so states could design benefits to meet the needs of their populations.

It is important to understand that the principal changes to private insurance that EHB mandated were to increase availability of coverage for maternity, mental health and substance use disorders, and habilitative care. Therefore, one possible goal of modifying the EHB rule would be to restrict those benefits.

Origins of EHB

To ensure the ACA delivered on its promise of making health insurance accessible and affordable, the law needed to define what health insurance means. To do that, the ACA establishes a standard that involves the scope of benefits (the EHB) and the extent of financial protection against the cost of these benefits. The latter is defined in terms of actuarial value—the minimum percentage of costs that a plan would pay for an average plan member, as grouped in metal levels.

While the actuarial value of plans can vary from metal level to metal level, the EHB are the same across plans. The ACA could have allowed different benefits for different plans, letting consumers choose the package of coverage that best fit their needs. However, that flexibility could create havoc with risk pools, as, for example, men could choose plans that didn't offer maternity care. In addition, a uniform benefits package simplifies the consumer shopping experience.

Finally, EHB was intended to deal with state mandated benefits, which many economists argue are a factor in driving up healthcare costs. Therefore, the ACA requires states to pick up the costs of mandates in Marketplace plans that exceed the scope of benefits in the EHB package.

EHB in Practice

The ACA defines ten broad categories of services as EHB:

- Ambulatory patient services;

- Emergency services;

- Hospitalization;

- Maternity and newborn care;

- Mental health and substance use disorders, including behavioral health treatment;

- Prescription drugs;

- Rehabilitative and habilitative services and devices;

- Laboratory services;

- Preventive and wellness services and chronic disease management; and

- Pediatric services, including oral and vision care.

The law tasks the Secretary of Health and Human Services (HHS) with defining these in detail. The Obama Administration initially asked the Institute of Medicine (IOM) of the National Academies, now known as the Health and Medicine Division, to recommend how it should define EHB. The IOM's recommended process would have had HHS start with a budget and fit EHB into that budget. Ignoring this advice, HHS declined to define specific EHB and instead gave each state substantial leeway in defining EHB. The regulations allow states to set EHB in reference to their own private health plans or to the Federal Employee Health Benefit Plan. This approach was attractive to HHS for several reasons:

- It avoided HHS having to make controversial decisions about which benefits to include and exclude.

- HHS argued that most private sector benefit packages were similar, so allowing states flexibility would not create large differences across the country.

- Tying EHB to large private sector health plans could create natural flexibility as plans change or states choose new benchmarks.

- States could select reference plans that already included their state-mandated benefits to avoid paying for state mandates.

Over time, HHS needed to intervene to remedy ambiguities in its EHB rules, in areas such as habilitative services and prescription drugs.

How EHB Changed the Pre-ACA Status Quo

To assess options for the future, it is helpful to have a clear picture of what reformers are seeking to address. It is entirely possible that EHB critics view state control as an end goal and would adopt an EHB standard identical to the current standard, albeit by a different process. But if that were the only goal, it is unlikely that stakeholders would expend political capital.

It seems plausible then that changing the required benefits package is itself a significant goal. It seems a reasonable inference that critics oppose the changes that the EHB package made to the pre-ACA status quo for the individual and small-group markets. If the EHB increased the cost of coverage, it did so because it required benefits that were not typically included in individual and small-group coverage—maternity care, habilitation services, and pediatric oral and vision care. In addition, while some mental health or substance use services were covered in nearly every plan, the depth of coverage varied widely.

Given this view of pre-ACA benefits, the debate on EHB might be framed as a debate about whether individual and small-group coverage should be required to cover maternity care, habilitative services, pediatric dental and vision, and mental health and substance use disorder services, as well as whether this decision should be made at the state or federal level.

Pathways to Reform

In the short term, there are opportunities for the Trump Administration to administratively change EHB. Critically, it cannot eliminate entire categories of EHB without legislation.

One option is for HHS to give states even more flexibility. HHS could allow states to choose from a wider variety of reference plans, to select different reference plans for each of the ten EHB categories and to define their own EHB without reference to any plans at all. Finally, the new Administration could use its waiver authority under section 1332 of the ACA to approve a state alternative to the ACA's EHB rules.

In the longer run, more options present themselves. Legislation could scrap completely the statutory EHB requirements and leave it up to the states or health plans themselves to set their own benefit rules or have none at all. One area where this may be more likely is for the Medicaid expansion population, as has already been proposed in the AHCA. This would be consistent with the Administration's calls for more state flexibility in administering Medicaid.

Whatever course is taken, defining the benefits that are "essential" to good healthcare will remain a critical issue in any national decision on universal healthcare coverage. The debate around the extent of benefits that states or the nation as a whole wish to subsidize is key to watch as the country grapples once more with fundamental changes in healthcare policy.

back to top

Third-Party Payment of Premiums: Controversy and HHS Guidance

By John M. LeBlanc, Partner, Healthcare Litigation | Carri Maas, Partner, Healthcare Litigation | Andrew H. Struve, Partner, Healthcare Litigation

Since the passage of the Affordable Care Act (ACA), the payment of healthcare premiums by third parties has been the subject of controversy. As Congress develops its plan to repeal and replace the ACA, it is uncertain how third-party premium payments will play out. While some view it as a charitable means to address exigent situations, others view it as a serious threat to the stability of the ACA's risk pools.

HHS Guidance

In October 2013, the Department of Health & Human Services (HHS) determined that health plans sold in the individual market are not "Federal healthcare programs" and therefore not subject to the federal antikickback statute that prohibits the exchange of anything of value in an effort to induce the referral of federal healthcare program business. The antikickback statute generally prohibits healthcare providers, pharmaceutical manufacturers and other interested parties from directly paying enrollees' Medicare or Medicaid premiums or other cost-sharing.

HHS's conclusion that the antikickback statute did not apply to the individual market appeared to be an invitation for these types of premium and cost-sharing assistance payments. However, the following month HHS issued guidance encouraging insurers to reject third-party premium payments from hospitals, healthcare providers and commercial entities due to "significant concerns" that allowing third-party payment arrangements could skew the insurance risk pool and create an uneven field in the exchange marketplace. These concerns apply equally to risk pools in the commercial marketplace.

In response to this guidance, several charitable organizations cried foul. HHS then revisited the issue in February 2014 and clarified that insurers should accept premium and cost-sharing payments from certain federal and state government programs, Indian tribes, and tribal organizations. HHS also clarified that the concerns cited in November 2013 were inapplicable to private, not-for-profit foundations, provided that those foundations rendered premium assistance based upon financial status and did not consider health status, as well as that they provided financial assistance for the entire policy year.

Controversy: Steering Patients to Health Insurance Marketplace Plans

What if a private, not-for-profit foundation satisfied HHS's guidelines but received all of its funding from healthcare providers? And what if those same healthcare providers referred Medicare and Medicaid patients to their affiliated foundations for financial assistance in an effort to steer those patients to private health plans so they could get paid more for providing the same services?

Steering Medicare and Medicaid patients to ACA plans is precisely the conduct alleged in a federal lawsuit brought by UnitedHealthcare of Florida (United) against American Renal Associates Holdings Inc., currently pending in the United States District Court, Southern District of Florida (Case No. 9:16-cv-81180-KAM). In that case, United alleges that American Renal Associates engaged in a fraudulent scheme to convince Medicare and Medicaid dialysis patients to drop their government insurance and sign up for United plans, and allegedly referred patients to a charitable foundation to help pay their premiums. The charity at issue, the American Kidney Fund, maintains a program for paying dialysis patients' premiums which is funded by dialysis providers.

According to the complaint, American Renal Associates' scheme was purely profit-driven—while American Renal Associates received $300 or less per dialysis session from government payers, it billed United $4,000 per session. American Renal Associates denies the allegations in the complaint.

If true, the alleged conduct presents a potential conflict of interest. Dialysis providers contribute to the charity, the charity provides financial assistance so dialysis patients covered by Medicare and Medicaid can obtain private insurance, and the dialysis providers' reimbursement for treating those same patients increases. This conduct can undermine the insurance risk pool. When a third party pays the premiums only for people in poor health, the insurance pool skews toward people who need more expensive healthcare, and everyone pays more.

CMS Information Request Highlights Concerns

In August 2016, the Centers for Medicare and Medicaid Services (CMS) issued a request for information seeking public comment regarding inappropriate steering by providers and provider-affiliated organizations of Medicare and Medicaid patients to individual market plans for the purpose of seeking higher reimbursement rates. In its request for information, CMS expressed concern that such practices "not only could raise overall health system costs, but could potentially be harmful to patient care and service coordination because of changes to provider networks and drug formularies, result in higher out-of-pocket costs for enrollees, and have a negative impact on the individual market single risk pool."

CMS Issues Interim Final Rule

In response to its August 2016 request for information, CMS received over 800 public comments, and on December 12, 2016, CMS issued regulations in the form of an interim final rule barring renal dialysis facilities from making premium payments for individual market health plans without (1) disclosing to the insurer that a third-party payment will be made, and (2) obtaining assurance from the insurer that third-party payments will be accepted.

The story, however, continues.

Federal Court Blocks CMS Regulations

A federal court in Texas blocked the CMS regulations that were set to go into effect on January 13, 2017. In granting a preliminary injunction, the court found that CMS bypassed—without good cause—notice and comment periods required under the Administrative Procedures Act. So, for now, the CMS regulations cannot be enforced.

While the antikickback statute does not currently apply to health plans sold on the individual market, that could change. The current draft of the American Health Care Act of 2017 (AHCA) being considered in the House of Representatives provides that any programs that receive certain federal grant funding would be subject to the antikickback statute, and under AHCA those grants would most likely support the individual market. We will have to wait and see how this unfolds under the new administration. Whatever the future holds, the issue of third-party payment of premiums cannot be ignored. The right solution should carefully balance the legitimate interests of patients, providers and insurers, while protecting the risk pools of all healthcare markets.

back to top

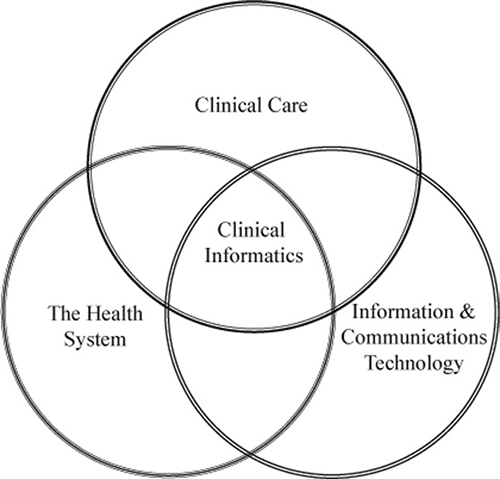

What Is Clinical Informatics?

By Alice (Ali) Loveys, MD, FAAP, FHIMSS, ABP-CI, Senior Advisor, Manatt Health

Clinical Informatics is defined by the American Medical Informatics Association (AMIA) as "the application of informatics and information technology to deliver healthcare services." The American Board of Medical Specialties first offered a board certification in this subspecialty in 2014. The creation of the new subspecialty is a response to exponential advances in health information technology (HIT) in private practices and hospital systems, as well as the increasing allocation of funds to support HIT adoption, implementation and optimization.

Who Are Clinical Informaticists—and What Do They Do?

Clinical informaticists are physicians who are board certified in a primary specialty and have completed a fellowship in clinical informatics or have substantial experience in the field. The physicians must pass a qualifying exam to be board certified.

What kind of work do clinical informaticists do? According to an article published in the Journal of Medical Information Association, "clinical informaticists transform healthcare by analyzing, designing, implementing, and evaluating information and communication systems that enhance individual and population health outcomes, improve patient care, and strengthen the clinician-patient relationship. Physicians who are board certified in clinical informatics collaborate with other healthcare and information technology professionals to promote patient care that is safe, efficient, effective, timely, patient-centered, and equitable."1

Clinical informaticists operate at the intersection of clinical care, the health system, and information and communications technology.

Building a Bridge Between End User Needs and Technologies

Clinical informatics evolved to meet the goal of bridging the clinical end user needs with available or developing technologies. Both areas have their own distinct "languages" and needed to find a way to talk to each other.

An essential building block of this bridge is an understanding of the set of communication standards developed by one or more Standard Development Organizations. These standards form an "alphabet soup" necessary for the standardized exchange of information. Some of the most recognizable standards include:

- Logical Observation Identifier Names and Codes (LOINCR)

- Digital Imaging and Communications in Medicine (DICOM)

- National Council for Prescription Drug Program (NCPDP)

- Health Level 7 (HL-7)

- International Classification of Disease Version 10 (ICD-10)

New standards continue to be developed as health systems grow, and the need for the exchange of information increases. For example, Fast Healthcare Interoperability Resources (FHIR—pronounced "fire") grew out of the need for a better interoperability standard between applications and electronic health records (EHRs).

A clinical informaticist understands that any one health system can be using a myriad of internal clinical applications, including EHRs, laboratory systems, billing systems and radiology systems. At the same time, a health system may need to interface with a plethora of external applications or systems. All of these systems need to be able to speak to each other and work together.

End users don't need to know about LOINC codes. They just want to know that the laboratory results appearing in their EHRs are captured accurately in analytic and reporting tools and can be successfully exchanged with outside applications such as portals or health information exchanges. They also need to be sure their systems achieve this goal in a way that complies with Health Insurance Portability and Accountability Act (HIPAA) Security and Privacy rules.

Clinical Informatics Drives Systemwide Confidence in Data and Technologies

In this era of value-based payments, population health analytics is at the forefront of applied health information technology. Each proposed technology must deliver on capturing and/or improving the quality of care a health system provides to its patients.

At the same time, the technology must enhance the clinical workflow, rather than impede it. With a clinical informatics approach, the clinical team can focus on fully understanding its workflow needs and identifying the best technology-enhancing services. Physicians are often skeptical about data derived from technology, unless they are involved in the process of determining how the data is sourced. An integrated, clinical informatics approach can assist the entire health system in gaining confidence in its data and technologies, driving continuous improvement.

1Source: J Am Med Inform Assoc. 2009;16:153–157. DOI 10.1197/jamia.M3045. Core Content for the Subspecialty of Clinical Informatics.

back to top

New Webinar: How Will Healthcare M&A Change Under the Trump Administration?

The healthcare M&A market continues to be among the most active sectors. In 2016, there were 939 healthcare industry deals in the U.S. with an aggregate value of approximately $71.7 billion.

How will policies and goals of the new administration likely impact healthcare M&A trends? How will changes in the regulatory landscape affect M&A across all healthcare stakeholder segments? What can you expect to see in terms of antitrust regulation and enforcement? Manatt addresses these and other key questions in a new webinar for Bloomberg BNA. The session will:

- Share an up-to-the-minute look at the status of ACA repeal and replace/repair efforts in Congress and the Executive Branch—and the implications of various scenarios on the healthcare sector.

- Analyze the conflicting policy goals and political dynamics driving the debate around the ACA.

- Review the changing landscape, critical issues and key takeaways for payer transactions, in the wake of the failed insurance megamergers.

- Examine hospital M&A and antitrust trends, including how the current climate might affect hospital transactions.

- Explore the issues around forming and operating Accountable Care Organizations (ACOs).

- Reveal the latest trends in state-action antitrust immunity for healthcare transactions.

- Anticipate how healthcare antitrust enforcement may change with a new administration.

- Present an update on regulatory and private antitrust activity in pharmaceutical pricing and pay-for-delay settlements.

Presenters:

Joel Ario, Managing Director, Manatt Health

Lisl Dunlop, Partner, Co-Chair, Antitrust and Competition

Tom Leary, Partner, Corporate and Finance

Eric Newsom, Partner, Chair, Corporate and Finance

back to top

Repeal of Antitrust Immunity for Insurers: What Does It Mean?

By Lisl J.Dunlop, Partner, Antitrust and Competition

Insurers are among a handful of industries, including Major League Baseball, that have a special exemption from the federal antitrust laws, the so-called "McCarran-Ferguson" antitrust exemption. The exemption has survived many repeal attempts, but—with the current focus on the high cost of health insurance and the need for greater competition in the healthcare industry generally—it appears finally to be reaching the end of its nine lives.

On February 28, 2017, the House Judiciary Committee voted to send to the full U.S. House of Representatives the Competitive Health Insurance Reform Act of 2017, H.R. 372, which would repeal the McCarran-Ferguson exemption. The House is expected to vote on the measure this month, ahead of the vote on the legislation to repeal and replace the Affordable Care Act (ACA). The article below discusses the genesis and scope of the McCarran-Ferguson exemption and what the repeal might mean for the healthcare industry.

Why Was the McCarran-Ferguson Exemption Created?

In 1944, the U.S. Supreme Court ruled that insurance companies were subject to the federal antitrust laws (since they acted in interstate commerce), and could therefore be prosecuted for anticompetitive conduct such as sharing competitively sensitive information with each other. Up until that time, insurance companies had regularly shared information to help determine risk levels and set appropriate premium prices on insurance policies.

In response to the Court's decision, Congress passed the McCarran-Ferguson Act in 1945, creating a limited exemption from the federal antitrust laws to allow insurance companies to share information with each other without the risk of antitrust liability. Under the law, regulating insurance company practices was left primarily to the individual states.

What Does the Exemption Do?

The McCarran-Ferguson Act grants an exemption from the federal antitrust laws to "the business of insurance" to the extent it is regulated by state law, unless the conduct involves an agreement or act to "boycott, coerce, [or] intimidate." Theoretically, under the exemption, insurers may be able to meet, share information and agree on pricing for premiums. Most states prohibit price-fixing by insurers, although enforcement has been uneven.

The law does not bar the federal government from regulating insurers or the industry entirely. The Federal Trade Commission (FTC) and the Antitrust Division of the Department of Justice (DOJ) remain responsible for antitrust enforcement involving mergers and acquisitions, as evidenced by the DOJ's challenges of Anthem's bid for Cigna and Aetna's offer for Humana. The DOJ also has challenged other conduct of insurers that may violate the federal antitrust laws, such as Blue Cross Blue Shield of Michigan's use of most-favored nations clauses that allegedly foreclosed rival health plans.

The principal activity that currently takes place under the exemption is the collection and pooling of claims data from different companies by "rating bureaus." Such information allows insurers to predict more accurately how much they might end up paying out to customers. These mechanisms are frequently used in industries such as property and casualty insurance.

Why the Repeal?

Proponents of the exemption, such as the Insurance Information Institute (III), say that the exemption is necessary to allow insurers to pool historic loss information, so they are better able to project future losses and charge an actuarially-based price for their products, as well as to allow for the joint development of policy forms. They argue that the sharing of such historical and trending data is needed, especially by smaller insurers that otherwise would be unable reasonably to assess risk and compete effectively. In the view of III, repeal of the exemption could result in increased premiums, as well as increase the risk of antitrust challenges and corresponding defense costs.

Proponents of repeal say that the legislation would spur competition among insurers and bring down costs for consumers. Further, proponents say that most of the activities conducted under the exemption—notably sharing of historical information to allow for risk assessments—would likely be permitted under the antitrust laws today. For example, collaborations in which data sharing takes place are assessed by antitrust enforcers and the courts under a rule of reason analysis that would fully consider the potential procompetitive effects of such conduct and condemn it only if, on balance, it was anticompetitive. To the extent that the activities are anticompetitive (such as premium price-fixing), such conduct should be condemned because it likely increases premiums in the marketplace.

How Would the Exemption's Repeal Impact the Healthcare Industry?

Many of those supporting repeal have focused on the healthcare industry as the major beneficiary. Reps. Tom Perriello, D-Va., and Betsy Markey, D-Colo., who are sponsoring the bill, said in a press release that it would "end special treatment for the insurance industry that allows them to fix prices, collude with each other, and set their own markets without fear of being investigated." House Judiciary Committee Panel Chair Rep. Bob Goodlatte, R-Va., said that the proposed law would "assist in Congress's larger goal of restoring competition to the healthcare industry and reversing the trend of rising payments and market consolidation."

It is unclear, however, whether the exemption has played a significant role in the health insurance business to date, and what impact repeal would have on competition in health insurance markets and health insurance premiums. An analysis by the Congressional Budget Office (CBO) estimated that repealing the antitrust exemption for health insurers "would have no significant effects on either the federal budget or the premiums that private insurers charged for health insurance."

Because there is such strong state regulation in the insurance arena, the repeal of the exemption may not have much practical effect. Further, if insurers lobbied the states, they could obtain the same or similar protections through state action, which can also act to shield conduct from the reach of the federal antitrust laws.

Conclusion

The repeal of the exemption continues to be the subject of debate, with some believing that it will boost competition and others arguing that it will have no real impact. A vote is imminent, and Manatt Health will continue to monitor the result, as well as the implications for healthcare, and keep you updated.

back to top

Escobar's Impact: Recent Application of "Materiality" in Ninth Circuit

By John M. LeBlanc, Partner, Healthcare Litigation | Andrew H. Struve, Partner, Healthcare Litigation | Katrina Dela Cruz, Associate, Litigation

Last year, a unanimous U.S. Supreme Court decided Universal Health Services, Inc. v. United States ex rel. Escobar (Escobar), 136 S.Ct. 1989 (2016), creating important implications for Federal False Claims Act (FCA) cases and, in particular, their viability. Generally, the FCA, 31 U.S.C. §§ 3729–3733, imposes liability on persons or entities who knowingly submit "false claims" for payment from federal funds or who improperly retain amounts received from the United States. Escobar endorsed one particular basis for liability under the FCA—the "implied false certification theory of liability," which holds that claimants impliedly certify compliance with certain statutes, regulations or contract requirements that are material conditions of payment, and therefore, that a claimant's failure to disclose any violation may render the claim false or fraudulent. The article below discusses Escobar's analysis regarding whether noncompliance is "material" under the FCA and the recent, subsequent application of the "materiality" standard by courts in the Ninth Circuit.

Brief Background on FCA Liability

Four elements are required to establish FCA liability: 1) a false statement or fraudulent course of conduct, 2) made with scienter, 3) materiality, and 4) causation. A "claim" can mean a direct request to the government for payment or a reimbursement request made to the recipients of federal funds under a federal benefits program, such as Medicaid. See 31 U.S.C. § 3729(b)(2)(A). The scienter requirement means the claimant must 1) have "actual knowledge of the [true] information," 2) "[act] in deliberate ignorance of the truth or falsity of the information," or 3) "[act] in reckless disregard of the truth or falsity of the information." 31 U.S.C. § 3729(b)(1)(A). The FCA also requires that the request be "material" to a false or fraudulent claim. 31 U.S.C. § 3729(a)(1)(B). "Material" means "having a natural tendency to influence, or be capable of influencing, the payment or receipt of money or property." 31 U.S.C. § 3729(b)(4).

Escobar addressed the "implied false certification theory of liability," which treats a payment request as a claimant's implied certification of compliance with relevant statutes, regulations or contract requirements that are material conditions of payment, and treats a failure to disclose a violation as a misrepresentation that renders the claim "false or fraudulent."

The Escobar Ruling

In Escobar, a teenage beneficiary of Massachusetts' Medicaid program received counseling services from a subsidiary of defendant Universal Health Services, Inc. (Universal). 136 S.Ct. at 1993. The teen had an adverse reaction to a medication prescribed by a purported doctor at the facility, and ultimately died of a seizure. Id. Her parents brought a qui tam action under the FCA upon discovering that some employees at the facility were not licensed to provide mental health counseling, not authorized to prescribe medications and not qualified to offer counseling services without supervision. Id. The lawsuit alleged that the facility's reimbursement claims to Medicaid amounted to "false claims" under an "implied false certification theory of liability." Specifically, the victim's parents alleged that Universal defrauded Medicaid by submitting reimbursement claims that made representations about services provided by individuals not qualified to render the services or who did not possess the required licensing. Id.

The district court granted Universal's motion to dismiss, holding that the parents failed to state a claim under the "implied false certification theory of liability" because none of the regulations allegedly violated by the facility constituted a condition of payment. Id. The First Circuit reversed, reasoning that (i) every submission of a claim for payment implicitly represents compliance with relevant regulations, therefore any undisclosed violation of a precondition of payment renders a claim false or fraudulent; and (ii) regulations themselves provide conclusive evidence that compliance was a material condition of payment. Id.

The Supreme Court vacated and remanded the case, albeit agreeing that the implied certification theory can be a basis for liability where at least two conditions are met: (i) the claim for payment makes specific representations about the goods or services provided, and (ii) the party's failure to disclose noncompliance with material statutory, regulatory or contractual requirements makes those representations misleading "half-truths." Id. at 2001. Further, for a misrepresentation about purported compliance with a statutory, regulatory or contractual requirement to be actionable under the FCA, the misrepresentation must be material to the government's payment decision. Id. at 2002. The Supreme Court noted that the FCA's rigorous materiality standard looks to whether knowledge of the noncompliance would have actually affected the government's payment decision.

Justice Thomas, writing for the Court, focused upon what can and cannot be considered material in this context. The Court explained that a misrepresentation is not necessarily material merely because the government designates compliance with a particular statutory requirement as a condition of payment (although such a designation is relevant). Nor, for that matter, is materiality conclusively established where the government would have had the option to decline payment if it knew of the party's noncompliance.

The Court instead turned the focus of the materiality inquiry to the party's knowledge and intended effect on the recipient, specifically "[w]hether the defendant knowingly violated a requirement that the defendant knows is material to the Government's payment decision." Id. at 1996. Proof of materiality could include evidence that the defendant knew that the government consistently refuses to pay claims based on noncompliance with the particular requirement. Conversely, if the government regularly pays a particular claim in full despite actual knowledge of noncompliance with a particular requirement, that is strong evidence that the requirement is not material.

Application of the Test for Materiality in the Ninth Circuit

Subsequent to Escobar, courts in the Ninth Circuit have displayed a measure of frustration with the Supreme Court's "guidance" on materiality. In September 2016, just five months after Escobar, one trial court in the Northern District of California pointed out potential conflicts from Escobar which focus the materiality inquiry on the likely or actual behavior of the recipient of the alleged misrepresentation. Rose v. Stephens Institute, Case No. 09-cv-05966-PJH, 2016 WL 5076214 (N.D. Cal. Sept. 20, 2016).

In Rose, relators brought a qui tam action against the Academy of Art University (AAU), alleging that the AAU fraudulently obtained funds from the U.S. Department of Education (DOE) by falsely alleging compliance with Title IV of the Higher Education Act, which generally prohibits any incentive payment based directly or indirectly on success in securing enrollments or financial aid to persons engaged in any student recruiting or admissions activities. 2016 WL 5076214, at *1. In its motion for reconsideration of the court's order denying summary judgment, the AAU argued that any noncompliance with the incentive compensation ban (ICB) was not material under Escobar.

The court, in denying the defendant's motion for reconsideration, concluded that the relators had raised a genuine issue of material fact as to materiality post Escobar. The district court recited the materiality factors: (i) whether the provision was a condition of payment, (ii) whether the government consistently refuses to pay claims in the mine run of cases based on noncompliance, or (iii) whether the government routinely pays a particular claim in full despite its actual knowledge of noncompliance. 2016 WL 5076214, at *6. In denying the motion for reconsideration, the district court found unpersuasive AAU's arguments that the DOE did not take any action against the AAU despite its awareness of the allegations in the case, and the DOE only rarely revoked a school's Title IV funds based on an ICB violation.

Another Ninth Circuit case, United States ex rel. Kelly v. Serco, Inc., 846 F.3d 325 (9th Cir. 2017) applied Escobar in its materiality analysis, and affirmed a district court's grant of summary judgment in favor of a government contractor, Serco. In Serco, a relator asserted that Serco violated material contractual requirements, because Serco's monthly cost reports allegedly did not comply with certain guidelines in the American National Standards Institute/Electronic Industries Alliance Standard 748 (ANSI–748).

In affirming the grant of summary judgment, the Ninth Circuit noted that the government did not rely upon Serco's cost reports in deciding whether to pay claims. The Ninth Circuit also paid particular attention to the reasoning in Escobar: "if the Government pays a particular claim in full despite its actual knowledge that certain requirements were violated, that is very strong evidence that those requirements are not material." 846 F.3d at 334. The Ninth Circuit noted that the government accepted Serco's cost reports despite knowing that such cost reports were not in compliance with ANSI–748.

Serco's adoption of the rigorous enforcement of the FCA's materiality requirement signals a limit to the implied certification theory following Escobar. This point is underscored through Ninth Circuit's explicit statement that courts can properly dismiss an FCA claim on summary judgment or a motion to dismiss based on the claimant's failure to meet the rigorous standard for materiality under the FCA.

Conclusion

As health insurance companies have increasingly been the targets of qui tam suits stemming from the application of the FCA to Medicaid payments to health insurers, the Supreme Court's ruling in Escobar is significant. It is no longer sufficient to demonstrate materiality by establishing that the government would have had the option to decline payment if it knew of the party's noncompliance. Nor would a simple showing of noncompliance with statutory, regulatory or contractual requirements be considered automatically material. Rather, it must be established that noncompliance would have actually affected the government's payment decision.

back to top

Now on Demand: "How Will the Trump Administration Impact Healthcare Litigation?"

Click Here to View the Program Free, on Demand—and Here to Download a Free Copy of the Presentation.

Donald Trump has vowed to eliminate the Affordable Care Act (ACA)—and the repeal and replace process has begun. Whatever the final outcome—whether an outright repeal or a partial rollback—significant changes would be triggered in existing healthcare law. How will healthcare litigation be affected? Manatt's new webinar for Bloomberg BNA provides the answer—and we want to make sure you don't miss out on this critical information.

If you or anyone on your team couldn't attend the webinar, click here to view it free on demand. If you would like a free copy of the presentation for your continued reference, click here.

The webinar begins with an analysis of the current state, setting the context with a detailed update on politics, policies and procedures. It then delves into how coming changes will affect healthcare litigation across a wide range of critical areas. Topics include:

- The Trump administration's healthcare positions, policies and priorities—including what we've seen in the first weeks and what's likely to come.

- The latest update on repeal and replace options, strategies, and efforts.

- Potential legislative and administrative actions and their impact by type of market, as well as by stakeholder group.

- The impact of eliminating or rolling back the ACA on healthcare litigation.

- The ways that current lawsuits challenging denials of access to care will be affected by partial or complete repeal.

- How existing litigation around coverage of services—such as contraception and transgender surgeries—is likely to move forward under other federal and state laws.

- If and how repeal and replace would affect other key litigation areas, such as fraud and abuse and pharmaceutical litigation.

If you have any questions or issues specific to your organization that you'd like to discuss, please reach out to our presenters:

back to top

Now on Demand: "What Are the Potential Implications of Capping Federal Medicaid Funding?"

Click Here to View Manatt's Recent Webinar Free, on Demand. Click Here to Download a Free Copy of the Presentation.

Key leaders in Congress and high-ranking members of the Trump Administration are proposing major changes to Medicaid financing through the adoption of a block grant or per capita cap. (The proposed American Health Care Act (AHCA) would convert Medicaid financing from the current guaranteed matching rate structure to a new per capita cap applied to virtually all spending under the program.) On March 8, Manatt Health presented a new webinar providing an overview of fixed funding proposals, using data prepared by Manatt Health for the Robert Wood Johnson Foundation State Network. The session also explained how to use the state-by-state Medicaid enrollment and expenditure data to assess the potential implications of proposals to cap federal Medicaid funding.

If you or anyone on your team were unable to attend the program—or want to view it again—click here to access it free, on demand. To download a free PDF of the presentation for your continued reference, click here.

Key topics covered during the webinar include:

- Explanations of block grants and per capita caps.

- The major elements of fixed funding proposals, including spend levels, trend rates and context-setting data.

- A review of the publicly available data included in the state-by-state data tables.

- Key drivers of base funding.

- Data and implications around state-level variations in Medicaid enrollment, spending and growth; new adult enrollment; federal funding; covered services and payment rates; use of supplemental payments; spending by eligibility group and per enrollee; and uninsured rates.

- An analysis of how fixed funding affects the risk to states.

- Medicaid's role in state budgets.

If you have any questions or issues you'd like to discuss, please contact our presenters:

back to top

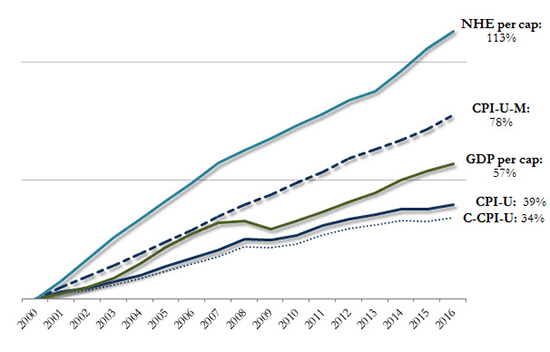

Decimals Matter: The Astounding Impact of Trend Rate Caps in Medicaid Funding Proposals

By Kevin McAvey, Senior Manager, Manatt Health | April Grady, Director, Manatt Health

The American Health Care Act (AHCA), currently under consideration by Congress, would cap future federal payments for most Medicaid beneficiaries by the growth in the medical component of the Consumer Price Index for Urban Consumers (medical CPI-U or CPI-U-M). Like its broader CPI parent, medical CPI measures price inflation for a select basket of goods and services over time; other variations include chained CPI, which allows for substitutions within the basket over time.

These CPI measures, as well as others that include U.S. Gross Domestic Product (GDP) and the Centers for Medicare and Medicaid Services' (CMS's) National Health Expenditures (NHE), have all been considered for use as trend rate caps in recent Medicaid reform discussions, drafts and bills. Understanding these measures, their data and reporting limitations, their relationship to Medicaid, and their historical and prospective growth rates (Figure 1) is critical to understanding the far-reaching impact their use could have on program spending, administration and state policy-making.

Figure 1: General Benchmark Growth, Cumulative (2000–2016)

Sources: Manatt Health analysis of: Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Expenditure Data; Bureau of Labor Statistics, CPI Databases; Bureau of Economic Analysis, National Economic Accounts, Gross Domestic Product Data.

Notes: Data shown on a calendar year basis.

The Impact of Using Benchmarks to Govern Spending

The use of benchmarks to regulate public program spending is not new to federal legislation. Since 1975, for example, Social Security and Supplemental Security Income have had automatic cost-of-living adjustments based on changes in CPI.i Advocates argue that using benchmarks to govern spending growth insulates future spending increases from public debate, maintains benefit levels, introduces predictability for federal spending and program administration and can generate significant federal long-term savings, as differences between projected and capped spending scenarios rapidly compound.

The Congressional Budget Office (CBO) highlights such savings potential from use of the medical CPI-U in its AHCA scoring:

"The limit on federal reimbursement would reduce outlays because (after the changes to the Medicaid expansion population have been accounted for) Medicaid spending would grow on a per-enrollee basis at a faster rate than the CPI-M…an average annual rate of 4.4 percent for Medicaid and 3.7 percent for the CPI-M over the 2017-2026 period. With less federal reimbursement for Medicaid, states would need to decide whether to commit more of their own resources to finance the program at current-law levels or whether to reduce spending by cutting payments to healthcare providers and health plans, eliminating optional services, restricting eligibility for enrollment, or (to the extent feasible) arriving at more efficient methods for delivering services. CBO anticipates that states would adopt a mix of those approaches, which would result in additional savings to the federal government."ii

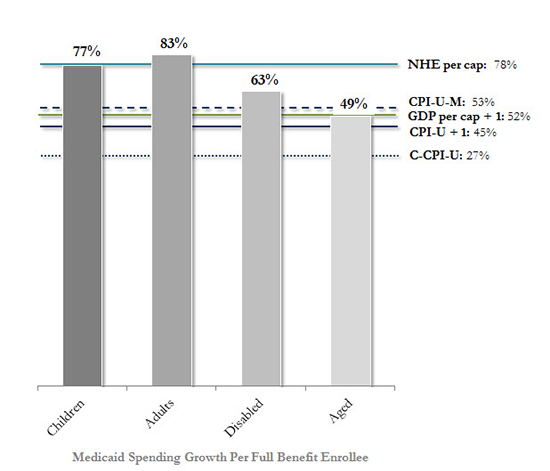

The CBO projects that Medicaid coverage-related provisions in the AHCA, including the medical CPI caps on Medicaid per beneficiary spending growth, would reduce direct federal Medicaid spending by $880 billion from 2017 to 2026. The extent to which savings can accumulate from relatively small annual percentage point differences (Figure 2) is clearer when viewing the cumulative impact from compounding (Figure 3).

Figure 2: Average Annual Growth Rates, Benchmarks & Medicaid Full Benefit Enrollee Spending (2000–2011)

-Bar-Graph.jpg)

Figure 3: Cumulative Growth, Benchmarks & Medicaid Full Benefit Enrollee Spending (2000–2011)

Sources: Manatt Health analysis of: Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Expenditure Data; Bureau of Labor Statistics, CPI Databases; Bureau of Economic Analysis, National Economic Accounts, Gross Domestic Product Data; Kaiser Family Foundation, Average Growth in Annual Medicaid Spending from FY 2000 to FY 2011 for Full-Benefit Enrollees.

Notes: Benchmark data shown on a calendar year basis; Medicaid data on a federal fiscal year. Medicaid enrollees were identified as having full benefits if for each month they were enrolled in Medicaid they also received full benefits or received Medicaid benefits through an alternative package of benchmark equivalent coverage. FY 2000–2011 data is displayed because this is the most recent period for which spending per enrollee levels and historical growth rates are calculated by Medicaid eligibility group using consistent data and methods across states in a publicly available analysis. Due to the shift in drug costs for the dually eligible from Medicaid to Medicare Part D as of 2006, prescription drug spending was excluded when calculating the average annual growth rate for aged enrollees.

Manatt Health's work with states, including Texas, Montana and Massachusetts has highlighted such considerations for local programs, while Manatt Health's Data "Toolkit for States," produced for the Robert Wood Johnson Foundation, empowers the public to make its own assessments.

Potential Savings and Risks

While the use of benchmarks to cap trend rates has the potential to produce savings, each carries its own risks. AHCA's use of medical CPI, for example, would require states to meet spending targets not finalized until the end of the spending period. Further, medical CPI, by design, may not trend to actual Medicaid expenses. Medical CPI, as a component-weighted approximation of "what households spend out-of-pocket on goods and services used for day-to-day living," does not necessarily represent those goods and services consumed by the Medicaid population, nor is it measured from the Medicaid population. As stated by the Bureau of Labor Statistics: The weights in the CPI do not include employer-paid health insurance premiums or tax-funded healthcare such as Medicare Part A and Medicaid.

Proposed Medicaid spending trend rate benchmarks would have a substantial impact on the amount of funding available to states, and their continued ability to finance coverage for more than 70 million individuals. This makes consideration of their impact, practicality and program relevance all the more important.

iBased on another CPI variant, called the CPI for Urban Wage Earners and Clerical Workers (CPI-W).

iihttps://www.cbo.gov/sites/default/files/115th-congress-2017-2018/costestimate/americanhealthcareact.pdf

back to top