Securing the Safety Net for America's Vulnerable Populations

By Cindy Mann, Partner, Manatt Health | Carol Raphael, Senior Advisor, Manatt Health | Stephanie Anthony, Director, Manatt Health | Keith Nevitt, Consultant, Manatt Health

Editor's Note: America's population is aging rapidly. By 2029, 75 million baby boomers will have reached age 65 and older, and older adults will represent more than 20% of the U.S. population. Many older people are poor or have insufficient savings or incomes for retirement. Medicaid is the default payer and provider for many of the long-term services and supports (LTSS) needed by the growing number of older Americans with low incomes and limited resources. The new administration must address the looming challenges that threaten Medicaid's ability to protect elders and fulfill its assumed responsibility for LTSS. In a new article for the Winter 2016–17 edition of Generations—Journal of the American Society on Aging, summarized below, Manatt Health presents seven strategies to preserve and strengthen Medicaid and create new financing options for delivering LTSS to low-income elders. Click here to download the full article free.

____________________________________

A Bleak Outlook for Older Americans

Many older Americans have insufficient income and assets to protect them through retirement. They often rely on Social Security (SSA) for retirement income, but Social Security only provides an average of $16,000 per year for retired workers. Many do not qualify for Social Security or receive very small Social Security payments and rely on Supplemental Security Income (SSI), which provides monthly benefits well below the Federal Poverty Level (FPL).

In addition, almost half of retirees surveyed in the 2016 Retirement Confidence Survey reported having less than $10,000 in savings and investments. Lack of savings will present a major challenge for people as they age. As of 2013, the median savings for Americans between ages 55 and 65 was only $14,500. Estimates show, however, that couples who retire at age 65 will require $260,000 for health costs alone during retirement.

Almost all older adults have Medicare coverage, but Medicare has gaps (most notably for LTSS) and substantial out-of-pocket costs. Those with low incomes are "dually eligible" for both Medicare and Medicaid. Those who reach 65 without enough work history to qualify for Medicare will rely on Medicaid for both their healthcare and LTSS coverage.

Older Americans living below 75 percent of the FPL (about $13,000 a year for a couple) automatically qualify for Medicaid in most states. Some of those not eligible for Medicaid when they turn 65 become eligible as a result of spending down their savings or income to cover medical expenses. In the absence of other public and private financing options for LTSS, Medicaid assumes the role of default payer of these costly services for six million elders. In 2014, total federal and state Medicaid LTSS spending was $152 billion, or a third of total Medicaid expenditures.

A Seven-Point Action Plan

The new administration must address the looming challenges that increasingly threaten Medicaid's ability to protect older adults. Below are seven actions that the new President can take not only to ensure greater economic and health security for our nation's older Americans and their families but also to preserve Medicaid as a critical safety net for our most vulnerable citizens.

Action 1: Ensure Medicaid is adequately funded and preserved as an entitlement program. Today's elders are living longer than ever before, with the average number of people ages 100 or older rising 43.6% between 2000 and 2014. People are also living longer with chronic illnesses and various forms of dementia, increasing the need for costly LTSS. To preserve Medicaid, the President must ensure sufficient funding and reject proposals that reduce or cap the federal government's responsibility to share in financing the program. Such initiatives would destabilize a 50-year-old cost-effective health insurance program; threaten the financial and health security of millions of older people who rely on Medicaid for LTSS; and increase pressure on states and the providers, health plans and somewhat fragile workforce that depend on Medicaid reimbursement.

Action 2: Advance proposals that automatically trigger an increase in federal Medicaid contribution during economic downturns. Medicaid was intentionally designed as a safety net for people in need and as an entitlement program for people who satisfy eligibility requirements. Enrollment is expected to (and does) grow during recessions, as people lose jobs, health insurance and savings. Increased federal Medicaid support is critical for states, especially during stressful economic times.

The federal matching assistance percentage (FMAP) is the percentage rate used to determine the federal matching funds allocated to states for Medicaid expenditures. The FMAP calculation is prescribed by federal law but, in general, can be no lower than 50 percent and no higher than 63 percent, and varies based on the relative wealth of each state. Congress has enacted numerous exceptions to the regular FMAP calculation, authorizing higher FMAPs to states in up to 20 circumstances, including two after the September 11 terror attacks. While these temporary adjustments have documented value, they are not guaranteed and, even when enacted, they may not be initiated soon enough to prevent damage and may end too quickly for many of the affected states. The President should call for an FMAP formula that is automatically increased without congressional action during times of economic stress.

Action 3: Increase awareness of LTSS needs and support creation of viable financing options. The need for LTSS will be a fact of life for more than half of those retiring today, yet few people reach old age prepared to deal with or pay for it. Only half of people ages 40 or older even know where to go for information. Additionally, most people are unaware of their financing options. Many mistakenly assume Medicare will pay for their LTSS needs, even though it only covers short-term nursing, home health and therapy services after a hospital stay. To complicate matters, the private insurance market for LTSS coverage is unraveling as premiums continue to rise while benefits shrink.

The President should support enhanced federal efforts through the Centers for Medicare & Medicaid Services (CMS) or the Administration for Community Living to increase awareness of people's lifetime LTSS needs. The President should also champion the creation of more viable and affordable LTSS financing options.

Action 4: Create a national family caregiver strategy. More than 80 percent of Americans who need LTSS receive it from informal caregivers (i.e., family members) and more than 40 percent of Americans ages 40 and older report having provided LTSS to family or friends. Family caregivers, the backbone of the LTSS workforce, contributed nearly half a trillion dollars' worth of unpaid care in 2013. Family caregivers experience high levels of emotional stress and financial strain and, as the population ages, the number of potential family caregivers is rapidly declining. Failure to support family caregivers adequately could result in increased pressure on Medicaid to provide care in their place.

The President should spur the creation of a national family caregiver strategy by advancing reforms that not only recognize the important role family caregivers play but also provide much needed financial and emotional support. To begin, the President should prioritize increasing awareness of existing tax incentives for family caregivers and explore strengthening them or creating new ones. The President also should support programs and initiatives that connect family caregivers directly to dedicated care coordinators.

Action 5: Support and enhance the direct care workforce. Demand for LTSS is increasing so rapidly that it is estimated that the direct care workforce will add 1.6 million new jobs by 2020 and become the largest occupational group in the country. However, direct care workers face many challenges, including low wages, lack of affordable housing and lack of training, leading to the rate of those leaving the occupation outpacing those entering. A strong workforce is key to providing quality care and helping individuals avoid expensive hospital visits or re-admissions.

At a minimum, the President should support proposals to articulate and ensure minimum training standards for direct care workers. The President also should support efforts to increase and stabilize direct care workers' earnings. Advocacy to increase wages also must promote steady hours and more predictable work schedules.

Action 6: Develop a core set of LTSS-specific quality metrics. Because LTSS span a multitude of care settings, provider types and payment structures, the healthcare industry has struggled to create meaningful quality metrics. The lack of meaningful measures results in a lack of comparable information, which consumers and policymakers need to make informed decisions.

The President should encourage consumer groups, providers, health plans, caregivers and other stakeholders to come together and develop a core set of meaningful quality metrics. These metrics must include both clinical and nonclinical measures to be standardized (to the extent possible) and connect to existing population health and hospital quality improvement measures. The President also must work with states to create a streamlined, straightforward and regularly updated dashboard that includes a manageable number of publically accessible metrics on LTSS quality.

Action 7: Challenge CMS and the private sector to develop care delivery innovations that include LTSS. To date, LTSS providers have generally been left to operate in a fee-for-service environment, largely disconnected from the rest of the healthcare continuum. Care fragmentation continues even in states that have moved LTSS into broader Medicaid managed care arrangements. The President should challenge CMS and the private sector to develop innovative care delivery and payment models that improve care quality while containing cost growth. In addition, the President should spur innovation in new technologies to support people in their homes, reducing the need for intensive face-to-face visits. Finally, the President should encourage the development of new independent and supportive housing alternatives.

Conclusion

Given that many people approaching retirement find themselves in challenging economic circumstances, the President must support proposals and initiatives that preserve and strengthen Medicaid, as it is the primary source of LTSS coverage for low-income adults. Doing so will give all older Americans health and financial security—and greater peace of mind.

back to top

Leveraging CHIP to Protect Low-Income Children From Lead

By Cindy Mann, Partner, Manatt Health | Kinda Serafi, Counsel, Manatt Health | Arielle Traub, Manager, Manatt Health

Editor's Note: Despite dramatic improvements over the past few decades, lead poisoning continues to be a serious hazard for many children in the U.S., presenting significant risks to their health and learning. The Children's Health Insurance Program (CHIP) can provide critical financial support to states and local communities that often face financing challenges as they seek to implement cost-effective lead abatement activities. In a new issue brief for the Robert Wood Johnson Foundation's State Health and Value Strategies Program, Manatt Health describes the CHIP State Plan option (no waiver required) and the opportunity it provides for states to significantly reduce lead exposure and improve children's health. The issue brief is summarized below. Click here to download a free copy of the full brief.

______________________________________________

More than four million families with children live in homes with high levels of lead and approximately half a million children under the age of five have blood lead levels above the recommended level. Lead exposure can cause serious physical and neurological damage to children. Even low levels of lead exposure can impact children's brain development and may result in reduced IQs, shortened attention spans or hearing and speech problems. Lead exposure also can cause anemia, hypertension, renal impairment, immunotoxicity and toxicity to reproductive organs. Low-income children, many of whom live in older housing, are particularly vulnerable to lead exposure. Research has shown that lead abatement efforts can yield significant cost savings through a range of societal benefits.

Under a long-standing but relatively under-utilized CHIP provision—known as the health services initiative (HSI)—states can leverage federal funding to develop and implement health initiatives for low-income children, including those that support lead exposure testing, prevention and abatement. To date, 19 states have received approval for CHIP HSIs for a variety of child health initiatives.

Opportunity to Use CHIP Funding to Combat Lead Poisoning

Title XXI of the Social Security Act—the federal authority for CHIP—provides states with a unique opportunity to access federal funds that they can use in targeted ways to reduce children's exposure to lead. Under the statute, states have the option to draw down federal matching funds at the enhanced CHIP rate for certain noncoverage expenditures, as long as those expenditures do not exceed ten percent of the total amount that a state spends on CHIP health benefits.

The noncoverage activities that are eligible for the CHIP federal matching rate include administrative costs related to the operation of CHIP, as well as expenditures for HSIs targeted at improving the health of low-income children. As CMS recently confirmed in its Frequently Asked Questions (FAQs) on HSIs, lead exposure and abatement programs aimed at low-income children are an authorized use of HSIs under CHIP authority.

Importantly, the CHIP matching rate for approved expenditures has always been higher than the Medicaid matching rate—and the Affordable Care Act (ACA) increased the Federal Medical Assistance Percentage (FMAP) for CHIP expenditures (including HSIs) by 23 points through September 30, 2019, making the minimum CHIP FMAP rate 88 percent in Fiscal Year 2017. Therefore, with relatively modest investment, states can draw down federal funds for HSIs up to the limit for noncoverage expenditures, creating an opportunity to make significant headway on lead testing, prevention and abatement for low-income children.

CHIP HSI SPA Process

The option to secure a CHIP HSI is part of the CHIP state plan template that states must complete and submit as they would for any other CHIP State Plan Amendment (SPA). Before submitting an HSI SPA to the Centers for Medicare & Medicaid Services (CMS) for approval, a state should develop a proposed lead abatement initiative and determine the funds available for an HSI lead abatement program. As long as the state keeps its noncoverage costs (i.e., administrative expenditures and HSI spending) within the ten percent limit, its expenditures for the approved HSI will be matched at the applicable CHIP matching rate.

Once a state determines the availability of funding for its HSI, it has considerable flexibility in designing a lead abatement program to meet the needs of low-income children younger than 19. States do not need to:

- Seek a waiver;

- Limit the initiative to children enrolled in Medicaid/CHIP, as long as the HSI targets low-income children (though guidance encourages states to enroll eligible children);

- Operate the HSI statewide; or

- Have a separate CHIP program. (States with CHIP-funded Medicaid expansions can receive HSI funding.)

To receive HSI funding for lead poisoning prevention and abatement, however, states must:

- Demonstrate the need for HSI;

- Describe an HSI proposal that is targeted at improving the health of low-income children;

- Identify source(s) of state share funding;

- Estimate the number of low-income children who will be served;

- Include a clearly defined timeframe for the initiative; and

- Meet the defined program design criteria (such as ensuring the individuals performing abatement services are state certified, among other criteria defined in CMS's recent FAQs).

Overview of State HSI Activities

Currently, 26 HSI SPAs are approved in 19 states, including Michigan which is using the HSI option to fund programs that support lead hazard detection, abatement and prevention. Some states focus primarily on projects to support statewide poison control centers that provide 24-hour emergency telephone treatment advice, referral assistance and information to manage exposure to poisonous and hazardous substances with respect to low-income children. Other states use the HSI funding to support a myriad of other initiatives, including supporting school health services, home visiting for at-risk newborns and their parents, and smoking cessation.

Given the urgent need to address lead exposure among low-income children, a targeted, effective strategy is essential for accomplishing state and local goals. No one strategy, however, is right for all communities. Each must find the optimal approach for its specific situation.

Conclusion

While CMS's HSI guidance is two decades old, states are only recently becoming aware of the opportunities to use HSI funding to support lead abatement activities. Given the considerable health, educational and societal risks associated with lead poisoning among low-income children, HSI funding presents a unique opportunity for states to stabilize and supplement existing funding for lead abatement activities and help prevent lead poisoning for the next generation of children.

back to top

New Webinar: How Will the Trump Administration Impact Healthcare Litigation?

Join Us on March 7 at 1:00 p.m. ET and Learn to Prepare for the Changes Ahead—and the Ramifications for Litigation. Click Here to Register Free—and Earn CLE.

Donald Trump has vowed to eliminate the Affordable Care Act (ACA)—and the repeal and replace process has begun. The Senate has introduced reconciliation instructions that leave most ACA provisions with a budget impact on the table. The debate continues to rage. Whatever the outcome—whether an outright repeal or a partial rollback—significant changes would be triggered in existing healthcare law. How will healthcare litigation be affected? Manatt's new webinar for Bloomberg BNA provides the answer.

The webinar begins with an analysis of the current state, setting the context with a detailed update on politics, policies and procedures. It then delves into how coming changes will affect healthcare litigation across a wide range of critical areas, from existing lawsuits around healthcare access and services to fraud and abuse litigation to federal vs. state regulation of health insurance. Click here to register free—and earn CLE. Key topics to be covered include:

- The Trump administration's healthcare positions, policies and priorities—including what we've seen in the first weeks and what's likely to come

- The latest update on repeal and replace options, strategies and efforts

- Potential legislative and administrative actions and their impact by type of market, as well as by stakeholder group

- The impact of eliminating or rolling back the ACA on healthcare litigation

- The ways that current lawsuits challenging denials of access to care will be affected by partial or complete repeal

- How existing litigation around coverage of services—such as contraception and transgender surgeries—is likely to move forward under other federal and state laws

- If and how repeal and replace would affect other key litigation areas, such as fraud and abuse and pharmaceutical litigation

Even if you can't make the original airing on March 7, click here to register free and receive a link to view the webinar free on demand.

Presenters:

Joel Ario, Managing Director, Manatt Health

Andrew Struve, Partner, Co-Chair, Healthcare Litigation

back to top

ACA Repeal Could Make Opioid Support Gains Short-Lived

By Valerie Barton, Managing Director | Kevin McAvey, Senior Manager | Jessica Nysenbaum, Senior Manager

In December, in rare and sweeping bipartisan action, Congress passed and President Obama signed the 21st Century Cures Act, legislation that included approximately $1 billion in critical financial support for states combating the opioid epidemic. However, researchers and public health advocates have since warned that the Act's provisions could be disproportionately overwhelmed, should the Affordable Care Act (ACA) be repealed without replacement. Opioid support gains the Act made possible would be vulnerable. Manatt Health's analysis confirms that an ACA repeal could leave many residents uninsured without access to care in states already experiencing the highest opioid death rates.

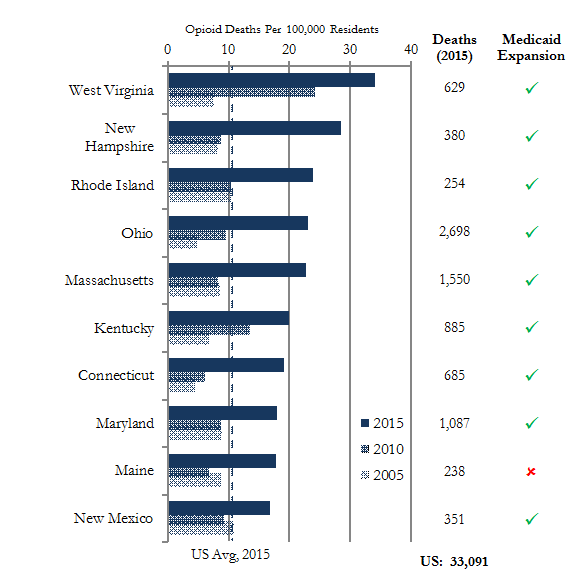

Using the latest data available from the Center for Disease Control's (CDC's) Multiple Cause of Death files, Manatt Health found that nine of the ten states with the highest opioid death rates in 2015 were at risk of losing coverage for their Medicaid-expansion populations (Figure 1), as well as for their large subsidized health exchange memberships. With health insurance coverage a lynchpin for access to evidence-based rehabilitation solutions such as medically assisted treatment, ACA repeal could leave patients without the necessary resources to fight addiction.

Over 33,000 people died in the United States from opioid-related drug overdoses in 2015, a 57% increase since 2010, and more than double the 2005 total (+122%). Ohio alone lost 2,700 residents to opioid overdoses; New York, 2,166; and California, 2,018. Nine other states lost more than a thousand lives. While West Virginia leads the nation in opioid-related deaths (34 per 100,000 residents), rates continue to increase in New Hampshire, Rhode Island, Ohio and Massachusetts, among dozens of other states, leaving policymakers across the country and the aisle acutely aware of the impact potential policy changes might have on states' abilities to address the epidemic.

Figure 1: States with Highest Opioid Overdose Death Rates (2015)

On January 11th, West Virginia Democratic Senator Joe Manchin stated that repealing the ACA without providing a replacement would "not only cause 184,000 West Virginians to lose their coverage," but would also result in "half of [the state's residents] in treatment [losing] their coverage that was made possible through the Affordable Care Act." Pennsylvania Republican Representative Charlie Dent concurred: "The impact of repealing the healthcare law without a pathway for reform or replacement on populations such as those suffering from substance abuse or mental health issues is one of the reasons I have urged…not to rush forward in initiating repeal efforts."

Manatt Health is currently advising several states with Medicaid behavioral health and substance abuse payment and delivery system reform agendas. For more information on Medicaid's role in battling the opioid epidemic, click here to download our recent issue brief, "Medicaid: States' Most Powerful Tool to Combat the Opioid Crisis."

Notes: Manatt Health analysis of Multiple Cause of Death File data using CDC developed opioid-related death specification.

Data Source(s): Centers for Disease Control and Prevention, National Center for Health Statistics, Multiple Cause of Death Files accessed via CDC Wonder Online Database.

Data Accessed: January 22, 2017

back to top

DOJ Successfully Blocks Insurance Mergers: What Are the Takeaways?

By Lisl Dunlop, Partner, Antitrust and Competition

In July 2016, following a lengthy review, the Antitrust Division of the Department of Justice (DOJ), together with several states, sued to block two proposed health insurer mergers: Aetna/Humana and Anthem/Cigna. On January 23 and February 8, two D.C. District Court judges issued decisions enjoining each of the transactions.

Although both transactions concerned health insurance markets, Judge John Bates, to whom both cases were initially assigned, ruled that there was little overlap in terms of parties, products, geographic markets and other factual issues, and in order to expedite the proceedings, separated the two cases. Judge Bates kept the Aetna/Humana case, in which the parties' agreement had a December 31 drop dead date, while the Anthem/Cigna case was assigned to Judge Amy Berman Jackson. This enabled hearings to take place in the late fall and decisions to be rendered early this year, a very quick six-month timeline for such complex matters.

Aetna/Humana

In a 156-page opinion, Judge Bates concluded that the proposed merger would likely substantially lessen competition in Medicare Advantage (MA) in all 364 counties that the DOJ listed in its complaint, as well as in the public exchanges in three counties in Florida. The court rejected the parties' efficiency claims, as well as claims that a proposed divestiture of MA plan assets to Molina would resolve competitive concerns.

Medicare Advantage Markets

As is customary in merger antitrust litigation, a key issue to be decided in the case was the appropriate definition of the relevant market. In this case, the main dispute was whether MA plans comprised a distinct market, or whether the market also should include original Medicare. The DOJ had consistently taken the position that MA plans were separate from original Medicare in earlier enforcement actions, but this was the first time the issue was considered by a court.

The court weighed the extensive evidence on the nature and extent of competition between original Medicare options and MA. The main sources of this evidence were the parties' documents and expert economic testimony. While acknowledging that some degree of competition exists between original Medicare and MA given their functional interchangeability, the court found industry and public recognition of a separate MA market. In particular, Aetna and Humana each segregated their MA businesses from other lines of Medicare business (Medicare Supplement plans), reported on MA market shares, and did not appear to take competition from original Medicare into account when pricing MA plans. The court noted that the parties' business documents were "ubiquitous" and "abundant" in focusing on competition within a separate MA market.

Competitive Effects in MA markets

Once the DOJ had established MA as a separate product market, it was able to show increases in concentration that led presumptively to the conclusion that the merger would lessen competition. The DOJ also introduced evidence of head-to-head competition between Aetna and Humana that has benefited consumers.

In response, the parties argued that government regulation, in the form of Centers for Medicare and Medicaid Services (CMS) rules and regulations around the MA bid process and tools, such as limits on medical loss ratios and margin and total beneficiary cost rules, would effectively prevent any attempt by the merged firm to act anticompetitively. The court disagreed, finding little ability for CMS to prevent the merged firm from increasing prices or reducing benefits.

The parties also argued that the threat of new MA entry into the counties in which the DOJ claimed competitive impact would be able to discipline post-merger conduct. Again, the court disagreed, referencing testimony that barriers to entry into MA markets are high, as well as economic evidence showing that entry was unlikely to be sufficient or timely enough to prevent a possible price increase.

Molina Divestiture

During the DOJ review period, Aetna and Humana had initiated a sale process for a set of MA plans that covered 290,000 members in 437 counties, including all the counties listed in the DOJ's complaint. Shortly after the complaint was filed, the parties entered into an agreement to sell the assets to Molina, a publicly-traded health insurance company with much of its current business in Medicaid. The court accepted that the Molina transaction should be considered in rebutting the DOJ's case, but ultimately found that the divestiture would not restore the competition lost by the proposed merger.

The parties argued that Molina had the capability to provide care management to lower income populations and build competitive provider networks, as well as the internal capacity to manage the MA plans, and would be able to use marketing and brokers to retain members. The court concluded that these arguments were undercut by documents authored by Molina board members and executives expressing skepticism about Molina's ability to execute the deals, in particular emails written while Molina's board was considering the deal to the effect that Molina did not have the resources, management and skills to manage the MA business it would be acquiring. The court also expressed concern at the low price Molina was paying for the assets, which "supports the conclusion that Molina has serious doubts about its own ability to manage all the divestiture plans, but is willing to try given the low risk to the company."

Competitive Effects in Public Exchange Markets

Although the anticompetitive impacts in 364 MA county markets would have been sufficient grounds on which to grant an injunction, the court went on to consider the DOJ's allegations that the merger would substantially lessen competition in public exchange markets in 17 counties in Florida, Georgia and Missouri. The market definition aspect of this part of the case was undisputed; the major disagreement was whether Aetna's withdrawal from those markets shortly after the complaint was filed mooted the government's case.

There was considerable debate over whether the reasons for Aetna's withdrawal from the exchanges mattered at all. Once Aetna had withdrawn, there was no competition to be lessened, and therefore, no antitrust concern. The court dismissed this argument, finding that there was nothing barring Aetna from deciding to re-enter the markets in question and compete in the future, and that it would be inappropriate to limit judicial inquiry in circumstances where the DOJ alleged that Aetna acted intentionally to evade judicial review.

The court held that there was adequate evidence in documents and testimony that Aetna had tried to leverage its participation in the exchanges for favorable treatment from the DOJ during the review period, and once it was clear the DOJ would move to block the merger went forward with plans to withdraw from the 17 counties in response. The court found that contemporaneous emails and documents ran counter to the argument that the withdrawal was a business decision and that underlying data concerning profitability in the Florida markets also supported the inference that withdrawal was litigation-related.

Ultimately, the court concluded that, given the profitability of its exchange business prior to withdrawal, Aetna would be likely to re-enter the three Florida exchange markets (but not the markets in Missouri and Georgia) and that the merger would reduce competition in those three markets.

Efficiencies

The parties claimed $2.8 billion in annual efficiencies arising from cost savings, including pharmacy rebate maximization, network medical cost savings and clinical services savings. The court expressed concern that a substantial portion of the efficiencies (approximately $2 billion) would likely be retained by the merged firm rather than be passed on to consumers, and that consumers actually harmed by the transaction (for example, MA plan purchasers) may not see any benefits from efficiencies. The court also analyzed favorably the DOJ's expert's criticisms of the companies' analyses of the potential efficiencies. Overall, the court found that the efficiencies did not reach the "extraordinary" level that would be required to mitigate the anticompetitive effects of the merger.

Anthem/Cigna

On February 8, Judge Jackson issued a 12-page Order enjoining the Anthem/Cigna merger, and also issued under seal a more detailed Memorandum Opinion. At the time of writing, the detailed opinion has not been unsealed, so the discussion below is based on the summary only.

National Accounts Market

The court accepted the DOJ's allegation that there was a separate market for large national accounts, defined as customers with more than 5,000 employees usually spread over at least two states. Although the Order describes the market as "the sale of health insurance to national accounts," it is clear that the companies are providing claims administration, claims adjudication and access to provider networks (ASO contracts), rather than insurance coverage. The Order also noted Anthem's and Cigna's separate business units for national accounts, and evidence that the industry as a whole recognizes national accounts as a distinct market.

The Order referenced witness testimony that there were only four national carriers offering the broad medical provider networks and account capabilities needed to serve a typical national account. Although the parties attempted to argue that customers have many alternatives and new entrants are poised to shake up the market, the court disagreed. The court noted that the barriers to entry are high, and although there are third-party administrators and new insurance ventures being launched by strong local healthcare systems, these typically do not have sufficient reach to meet the needs of a national account.

The court also rejected the parties' arguments that customers could slice up their businesses among multiple carriers to cover different geographic regions, finding that although this is theoretically possible, employers do not elect to do so very often. Even when national accounts do break up their business, they tend to use no more than two companies chosen from the big four national players and a strong regional player, such as Kaiser in California.

Although the Order discusses the needs of "national" accounts, the geographic market in which the court analyzed competitive effects was limited to the 14 states in which Anthem operates as the Blue Cross Blue Shield licensee. Because the court found anticompetitive impact in this market, it did not go on to consider the impact nationally, in an alternative market for the sale of health insurance to large group employers of more than 100 employees in the Anthem states, or in markets for the purchase of healthcare services from hospitals and physicians. Curiously, the Order does reference findings in relation to a specific large group market in Richmond, VA, even though this does not appear to be essential to the ultimate decision.

Efficiencies

As in the Aetna/Humana case, Anthem asserted that any anticompetitive effects would be outweighed by the efficiencies that would be generated by the merger. In addition to cost savings in general and administrative areas, Anthem contended that national account customers would save a total of over $2 billion in medical expenditures, because Cigna members would be able to access the more favorable discounts that Anthem had negotiated with its provider network, while Anthem members would benefit where Cigna had lower rates.

The court rejected the claimed medical cost savings as not merger-specific because they are based on "the application of existing discounts to an existing patient population." The court also questioned whether Anthem's ability to drive a hard bargain with providers by virtue of its size should even be considered an efficiency when the product that Anthem and Cigna are selling in the national accounts market is ASO contracts, not healthcare.

The court criticized other arguments Anthem made concerning the need to control growing healthcare costs as seeking to have the court make "complex policy decisions about the overall allocation of healthcare dollars in the United States." The court also noted other evidence about the potential difficulties in Anthem seeking to extend its discounted fee schedule to additional providers and facilities and the possible erosion of relationships between insurers and providers.

Cigna Evidence

The court noted that Cigna was "actively warned against" the merger, and referenced Cigna testimony undermining the efficiencies claims, Cigna cross-examination of the defendants' own expert and Cigna's refusal to sign Anthem's Findings of Fact and Conclusions of Law. Although Anthem urged the court to "look away" from the differences between the merging parties, the court found this evidence relevant to its decision.

The Order discusses Anthem's and Cigna's fundamentally different approaches to their healthcare strategy: Anthem believing that its greater ability to command discounts from providers will save its customers money and Cigna saying that its greater engagement and collaboration with providers will ultimately save customers money. The court concluded that these differences highlight the need to preserve the different options generated by such disparate approaches for customers.

Innovation

The Order also discusses Cigna's differentiation in providing better information and clinical management to lower utilization and achieve cost-savings over time. Some customers prefer this approach, notwithstanding Cigna's discount disadvantage, and there was testimony that the approach is working. The court held that permitting the merger would result in less opportunity for such ideas to be tested and refined, and lead to a loss of innovation in the industry.

Takeaways

To be sure, the government has been enormously successful over the past year in challenging mergers in the healthcare industry. From the Federal Trade Commission's successes in challenging two major hospital mergers to the DOJ's successful enforcement actions against the two health insurer mergers, the government has established itself as a serious hurdle for any major transaction.

The two insurer merger decisions highlight several aspects of the ways in which agencies win merger cases: the use of documentary evidence and the high bar required for the efficiency defense. The decisions also highlight the need for collaboration and consistency between merger parties.

Both opinions rely heavily on documentary evidence from the parties' files, notably ordinary-course business documents describing the industry and competitive landscape in which the parties operate. As Judge Bates' treatment of such material in considering whether MA is a separate market demonstrates, consistent references in company documents will outweigh subsequent testimony or post-announcement discussions of the markets that will be affected. A careful and honest appraisal of the documents a company already has in place is essential when considering a transaction.

Key evidence also included documents that directly contradicted the parties' trial positions and witness testimony on certain issues. While parties often receive advice on document creation when considering a transaction, such guidance is often too late for some important issues, and third parties cannot be controlled. Companies should consider including guidelines on company document creation in regular compliance and other briefings.

In addition, the decisions make it clear that, once the government establishes its prima facie case that competition will likely be adversely affected, it is very difficult to defend a transaction on the basis of potential efficiencies. While significant work appears to have been done in developing the efficiencies claims in the two insurance cases, both decisions set very high standards for the efficiencies to be cognizable, and overall appear quite hostile to the effectiveness of potential efficiencies in ameliorating anticompetitive impacts. When a transaction leads to significant concentrations and the agencies are skeptical of efficiency defenses in the review process, an efficiencies defense is unlikely to win the day in court.

Finally, it seems obvious that cooperation between merging parties is essential to putting on an effective defense of a merger case. Most merger agreements contain express provisions requiring such cooperation, and parties and counsel typically work side-by-side in sharing evidence and strategy and preparing presentations and arguments at all stages of the review process. Such collaboration also is essential to ensuring swift and effective implementation of the transaction once it has cleared regulatory hurdles.

back to top

HCQIA Preemption of State Physician Whistleblower Statutes

By Barry Landsberg, Partner, Healthcare Litigation | Doreen Shenfeld, Partner, Healthcare Litigation | Colin McGrath, Associate, Litigation

Medical professionals who are subject to adverse actions following peer review often seek to sue the peer review participants (including the individual peer-reviewing physicians, medical staff leadership and the hospital), casting themselves as quality-of-care advocates that have been mistreated or retaliated against for advocating for their patients or complaining about substandard care. Some states have enacted whistleblower protection statutes under which physicians can bring such cases and seek monetary damages. While few courts have addressed the issue, such statutes appear to be preempted, at least in part, by the federal physician peer review statute, known as the Health Care Quality Improvement Act of 1986 (HCQIA), 42 U.S.C. § 11101 et seq. This statute immunizes peer review participants from money damages stemming from peer review actions and proceedings unless the physician can establish that certain enumerated conditions have not been met. 42 U.S.C. §§ 11111, 11115(a).

HCQIA presumptively immunizes peer review participants and hospitals from damages claims stemming from objectively reasonable peer review actions1 in which the affected physician received or was offered an internal administrative hearing that meets certain fair hearing standards. HCQIA provides, in pertinent part:

If a professional review action (as defined in section 11151(9) of this title)2 of a professional review body meets all of the standards specified in section 11112(a) of this title3. . . :

(A) the professional review body,

(B) any person acting as a member or staff to the body,

(C) any person under a contract or other formal agreement with the body, and

(D) any person who participates with or assists the body with respect to the action,

shall not be liable in damages under any law of the United States or of any State (or political subdivision thereof) with respect to the action.

42 U.S.C. § 11111(a)(1) (emphasis added).

Congress enacted HCQIA in 1986 with the expressed intent to protect the public by improving the quality of professional peer review by (a) limiting money damage awards against peer reviewers; (b) providing incentives and other protections to peer reviewers; and (c) preempting any state law that provided fewer or lesser protections, incentives or immunities:

(1) The increasing occurrence of medical malpractice and the need to improve the quality of medical care have become nationwide problems that warrant greater efforts than those that can be undertaken by any individual State. (2) There is a national need to restrict the ability of incompetent physicians to move from State to State without disclosure or discovery of the physician's previous damaging or incompetent performance. (3) This nationwide problem can be remedied through effective professional peer review. (4) The threat of private money damage liability under Federal law . . . unreasonably discourages physicians from participating in effective professional peer review. (5) There is an overriding national need to provide incentive and protection for physicians engaging in effective professional peer review.

42 U.S.C. § 11101 (emphasis added).

HCQIA Balances Competing Interests

Consistent with this purpose, HCQIA provides that States may enact laws that provide the same or greater protections as HCQIA, but not lesser protections: "[N]othing in this subchapter shall be construed as changing the liabilities or immunities under law or as preempting or overriding any State law which provides incentives, immunities, or protection for those engaged in a professional review action that is in addition to or greater than that provided by this subchapter." 42 U.S.C. § 11115(a) (emphasis added). See also Patrick v. Burget, 486 U.S. 94, 105, fn. 8 (1988) (noting that HCQIA "allow[s] States to immunize peer-review action that does not meet the federal standard").

Courts have consistently held that state peer review immunity laws that provide less protections than HCQIA, or that impose more stringent requirements in order to receive the same protections, are preempted by HCQIA. See Wood v. Archbold Medical Center, Inc., No. 6:05-CV-53 (HL), 2006 WL 1805729, at *3 (M.D. Ga. June 29, 2006) ("Georgia Law generally provides immunity from criminal and civil liability unless the health care provider was motivated by malice. Georgia courts have consistently held, however, that 'to the extent that peer review immunity . . . is conditional upon the absence of motivating malice, it is preempted by the HCQIA.'"), quoting Patrick v. Floyd Medical Center, 255 Ga.App. 435, 444 (2002); see also; Goodwich v. Sinai Hosp. of Baltimore, Inc., 103 Md.App. 341, 354 (1995) (Maryland peer review immunity statute, Md.Code, Health Occ. art., § 15–402, "is preempted by [HCQIA] only to the extent that it provides less immunity than [HCQIA]" in requiring that a review committee member act in good faith) (emphasis in original).

Recent Case Examples From California

Outside the context of state peer review immunity statutes, however, the issue of HCQIA preemption has received far less attention.4 Two recent cases from California have acknowledged, without directly addressing, the issue of HCQIA preemption within the context of medical professional whistleblower protection statutes. The statute in question in both decisions, California Health and Safety Code Section 1278.5 ("Section 1278.5"), authorizes a physician to sue a hospital or medical staff for monetary damages5 stemming from the hospital or medical staff's "discriminatory treatment"6 of the physician. Cal. Health & Safety Code § 1278.5(b)(1), (g), (i). In Fahlen v. Sutter Central Valley Hospitals, 58 Cal.4th 655, 685–686 (2013), the California Supreme Court acknowledged the issue of possible preemption of Section 1278.5 by HCQIA, but it declined to address the issue "in detail" because it had not been raised in the lower courts. Instead, the California Supreme Court noted only that HCQIA does not "absolutely foreclose a state tort suit alleging that a peer review decision constituted improper retaliation against a whistleblower" because HCQIA does not preclude non-monetary remedies such as reinstatement and injunctive relief, and also because the presumption of immunity under HCQIA is rebuttable. Id. at 686. But whether HCQIA "absolutely foreclose[s]" tort claims against a peer review participant under Section 1278.5 is a separate question from whether Section 1278.5's authorization of monetary damages against a peer review participant is preempted by HCQIA—a question the California Supreme Court did not answer because the issue had not been raised by the parties in the lower courts.7

More recently, in Armin v. Riverside Community Hospital, 5 Cal.App.5th 810, 831–832 (Dec. 15, 2016), a California Court of Appeal similarly sidestepped the issue of HCQIA preemption of claims for money damages under Section 1278.5 arising out of hospital peer review proceedings. Like in Fahlen, Armin framed the question as whether the hospital was immunized from any claims brought under Section 1278.5. Id. at 831. This broad framing of the issue allowed the court to avoid confronting the preemption question directly; instead, the court simply followed in Fahlen's footsteps, stating that "HCQIA cannot provide blanket immunity to a hospital in a section 1278.5 action because even if HCQIA applies to a given peer review proceeding, 'at a minimum' it still allows 'such remedies as reinstatement and injunctive relief." Id. at 832, quoting Fahlen, 58 Cal.4th at 686. Whether California courts will continue to sidestep this question for damages claims brought under Section 1278.5 remains to be seen. It is an issue that courts must eventually decide, because many physicians suing under Section 1278.5 seek damages, not reinstatement of their privileges or merely equitable relief.

Whistleblower Protection in Other States

Looking beyond California, several other states also have whistleblower protection statutes for healthcare employees. For example, the Maryland Health Care Worker Whistleblower Protection Act, MD Code, Health Occupations, § 1-501 et seq., allows an employee physician to bring an action for money damages against a hospital if the hospital takes "any personnel action" against the physician as a result of the physician's whistleblowing. Id., § 1-502, 1-505(5), (6). Other states with similar healthcare employee whistleblower statues that authorize money damages in actions brought by an employee physician against a hospital include (but are not necessarily limited to): Illinois (210 ILCS 86/35, 86/40); New York (N.Y. Labor Law §§ 740, 741); and Texas (Health & Safety Code § 161.134). No court has addressed HCQIA preemption of any of these particular statutes, but there is a reasonable argument to be made that these statutes are preempted by HCQIA at least to the extent they authorize monetary damages against hospitals or physicians for claims stemming from peer review proceedings.

Conclusion

Although the issue of HCQIA preemption of physician whistleblower statutes has received very little attention by the courts, any state law that allows hospitals or physicians to be sued for monetary damages based on their participation in peer review proceedings is directly contrary to the express purpose of HCQIA and cannot reasonably be said to provide incentives, immunities or protections "in addition to or greater than" those provided under HCQIA. Accordingly, defense counsel should be prepared to make an HCQIA preemption argument in any case against a physician whistleblower claim under state law that seeks monetary damages against a hospital or other peer review participant.

1The case law applying HCQIA is virtually uniform that the statutory immunity from damages arising from peer review action is governed by a purely objective standard: Did the hospital and peer review committees reasonably investigate before acting, was the action taken reasonably in furtherance of patient care, and did the hospital provide fair hearing or other fair procedure to the physician? See 42 U.S.C. § 11113(a)(1)–(4). As such, the motive for taking corrective peer review action is irrelevant as a matter of law. See Austin v. McNamara, 979 F.2d 728, 734 (9th Cir. 1992) ("alleged animosity" and "assertions of hostility" by a physician "are irrelevant to the reasonableness standards of § 1111(a)); Fox v. Good Samaritan L.P., 801 F.Supp.2d 883, 890 ("Importantly, evidence of bad faith or hostility towards Fox on the part of the actual decision-makers is simply irrelevant and cannot serve to create a material issue of fact on this point."); Poliner v. Texas Health Sys., 537 F.3d 368, 379-80 (5th Cir. 2008) ("Our sister circuits have roundly rejected the argument that such subjective motivations overcome HCQIA immunity, as do we."); Wood v. Archbold Medical Center, Inc., 738 F.Supp.2d 1298, 1350 (M.D. Ga. 2010) ("courts all over the country have held that a plaintiff's 'urging of purported bad motives or evil intent or that some hospital officials did not like him provides no succor,'" as the inquiry under HCQIA is an objective one) (quoting Poliner); Brader v. Allegheny General Hosp., 167 F.3d 832, 840 (3d Cir. 1999) ("Like other circuits, we have adopted an objective standard of reasonableness in this context. Therefore, the good or bad faith of the reviewers is irrelevant."); Manzett v. Mercy Hosp. of Pittsburgh, 776 A.2d 938, 934 (Pa. 2001) ("In an HCQIA action, plaintiffs are not permitted to introduce evidence of bad faith of the participants in the peer review process.").

2"Professional review action" is defined, in pertinent part, as "an action or recommendation of a professional review body which is taken or made in the conduct of professional review activity, which is based on the competence or professional conduct of an individual physician (which conduct affects or could affect adversely the health or welfare of a patient or patients), and which affects (or my affect) adversely the clinical privileges, or membership in a professional society, of the physician." 42 U.S.C. § 11151(9).

3To qualify for immunity under Section 11111(a), the "professional review action must be taken— (1) in the reasonable belief that the action was in the furtherance of quality health care; (2) after a reasonable effort to obtain the facts of the matter; (3) after adequate notice and hearing procedures are afforded to the physician involved or after such other procedures as are fair to the physician under the circumstances; and (4) in the reasonable belief that the action was warranted by the facts known after such reasonable effort to obtain facts and after meeting the requirement of paragraph (3)." 42 U.S.C. § 11112(a). These standards are presumed to have been met unless rebutted by a preponderance of the evidence.

4But see Diaz v. Provena Hospitals, 817 N.E.2d 206, 212–213 (Ill.App.Ct. 2004) (HCQIA impliedly preempts state court order (1) preventing a hospital from submitting a HCQIA-required report and (2) holding hospital in contempt for having submitted it: "the substantial monetary penalty the court imposed on the Hospital as a result of its contempt finding qualifies as 'liability under state common law.' . . . Because it was impossible for the Hospital to comply with the HCQIA without being fined and held in contempt of court, the doctrine of implied preemption applies.").

5Section 1278.5 also authorizes non-monetary remedies, including reinstatement or, broadly, "any remedy deemed warranted by the court" under California law. Cal. Health & Safety Code § 1278.5(g).

6"Discriminatory treatment" for the purposes of the statute "includes, but is not limited to, discharge, demotion, suspension, or any unfavorable changes in, or breach of, the terms or conditions of a contract, employment, or privileges of the . . . member of the medical staff, . . . or the threat of any of these actions." Cal. Health & Safety Code § 1278.5(d)(2).

7That HCQIA immunity is limited to damages and does not preclude equitable relief is well established in federal courts across the country. See, e.g., Imperial v. Suburban Hosp. Ass'n, Inc., 37 F.3d 1026, 1031 (4th Cir. 1994) ("[T]he actual protection given by [HCQIA] is limited to damages liability. . . . [D]isciplined doctors [can] continue to bring 'private causes of action for injunctive or declaratory relief.'") quoting H.R. Rep. No. 903, 99th Cong., 2d Sess. 2, reprinted in 1986 U.S.C.C.A.N. at 6391; Sugarbaker v. SSM Health Care, 190 F.3d 905, 918 (8th Cir. 1999) ("HCQIA immunity is limited to suits for damages; there is no immunity from suits seeking injunctive or declaratory relief."); Cohlmia v. St. John Medical Center, 693 F.3d 1269, 1279 (10th Cir. 2012) (same); Gordon v. Lewiston Hosp., 423 F.3d 184, 191 fn. 1 (3d Cir. 2005) (same).

back to top

Now on Demand: What Does a Trump Administration Mean for Healthcare?

Click Here to View Manatt's Recent Webinar Free on Demand, and Here to Download a Free Copy of the Presentation.

On January 12, Manatt Health presented a new webinar examining what the Republican sweep of the presidency, House and Senate—as well as its control of 33 governorships and 70 of 99 state legislative bodies—means for healthcare at the federal and state levels. The program provides a detailed look at what to expect from the new Trump Administration.

If you or anyone on your team were unable to attend the session—or want to view it again—click here to access it free on demand. If you would like a free copy of the presentation for your continued reference, click here.

The webinar addresses a broad range of key issues:

- The Trump Administration's healthcare agenda and competing priorities

- The healthcare positions, goals and legislative/policy backgrounds of key appointees—and their potential impact

- Potential administrative and legislative actions in areas such as drug costs, Medicare, Medicaid, Marketplaces, reproductive health and employer coverage

- Policy options for "repeal and replace," including the key components of a replacement strategy

- Key events coming up this year—from the expiration of CHIP to decisions on the insurance company mergers to cost-sharing reductions and risk-adjustment payments

Federal Insights: New Manatt Publication with Ongoing Updates

Manatt recently launched a new publication, Federal Insights, which is designed to provide concise and timely updates on key health reform developments as they occur at the federal and state level. If you would like more information or to subscribe, please contact Chiquita Brooks-LaSure, Managing Director, Manatt Health.

back to top